Democratic members of the House and Senate introduced new legislation on Thursday to end what they call “Wall Street Looting.”

The “Stop Wall St. Looting Act” would create new rules for private equity firms that would prevent them from enriching themselves by charging management fees and passing on their debts to the companies they buy.

In theory, private equity firms are investment management companies that invest in or buy up businesses or start-ups for a mutually beneficial business arrangement.

What often happens in practice, however, is equity firms end up transferring debt to the companies they invest in, cutting hours, and cutting jobs in order to maximize profits while the companies they invest in are crippled or even shut down.

“Private Equity firms raise money from investors, kick in a little of their own, and then borrow tons more to buy other companies,” Senator Elizabeth Warren, a sponsor of the bill, wrote in an outline of the legislation on Medium.

“Sometimes the companies do well. But far too often, the private equity firms are like vampires – bleeding the company dry and walking away enriched even as the company succumbs.”

Private equity firms want you to believe you’re not smart enough to understand their business model. But it's pretty simple: take over companies & loot 'em.

And I’ve got a bill with @SenatorBaldwin, @SenSherrodBrown, @RepMarkPocan & @RepJayapal to fix it. #StopWallStreetLooting pic.twitter.com/wbz16jKpTG

— Elizabeth Warren (@SenWarren) July 18, 2019

The bill, which is being sponsored by lawmakers including Warren, Senators Tammy Baldwin and Kirsten Gillibrand, and Representatives Ro Khanna and Rashida Tlaib, would also hold firms responsible for pension and severance obligations to employees.

Further, it would change tax and bankruptcy rules, prevent lenders from making high-risk loans to companies in serious debt, and close the carried interest loophole that allows firm managers to pay lower tax rates on their profits from the companies they buy.

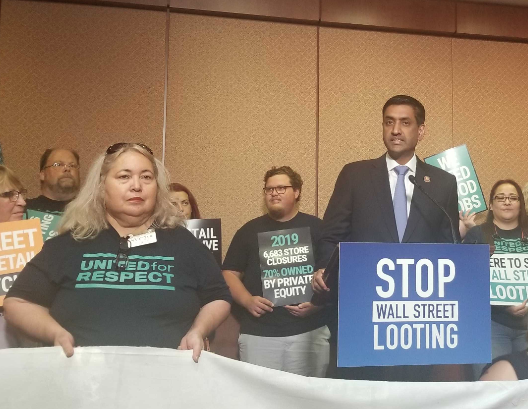

To announce the bill, members of Congress held a press conference in the Capitol visitor’s center alongside workers who have been affected by Wall Street firms which buy up companies only to lay off employees without promised severance in order to turn a profit.

Service industry workers shared their personal stories of hardship and journalists spoke about how this practice leads newsrooms to shut down after equity firms buy them up and create “news deserts” in local communities that have long been served by local news organizations.

Giovanna De La Rosa worked as a Toys R Us store manager in San Diego, California for 20 years and said she was directly affected by private equity after Kohlberg Kravis Roberts & Co. and Bain Capital bought out the company in 2005.

“They eliminated positions and hours were being cut,” De La Rosa told The Globe Post. “We went from being a mostly full-time store to nine to one part-time vs. full-time workers … it was all about numbers. Less hours and more sales. You could tell that the company did not care about the employees.”

De La Rosa said the store ultimately closed down after the company went bankrupt and despite being promised severance pay, she ended up not getting anything.

Speaking at the press conference, Khanna criticized equity firm investors for excessive profiteering from working-class Americans.

“If you talk to an ordinary person…they’ll say maybe someone who’s making an investment should make $50,000, $100,000, $500,000 even,” Khanna said. “But $50 million dollars? I mean who do these people think they are? …They’re paper shufflers. They’ve got an inflated sense of their contributions to the economy.”

More on the Subject

Dividends and Disaster: How For-Profit Utilities Threaten Public Safety